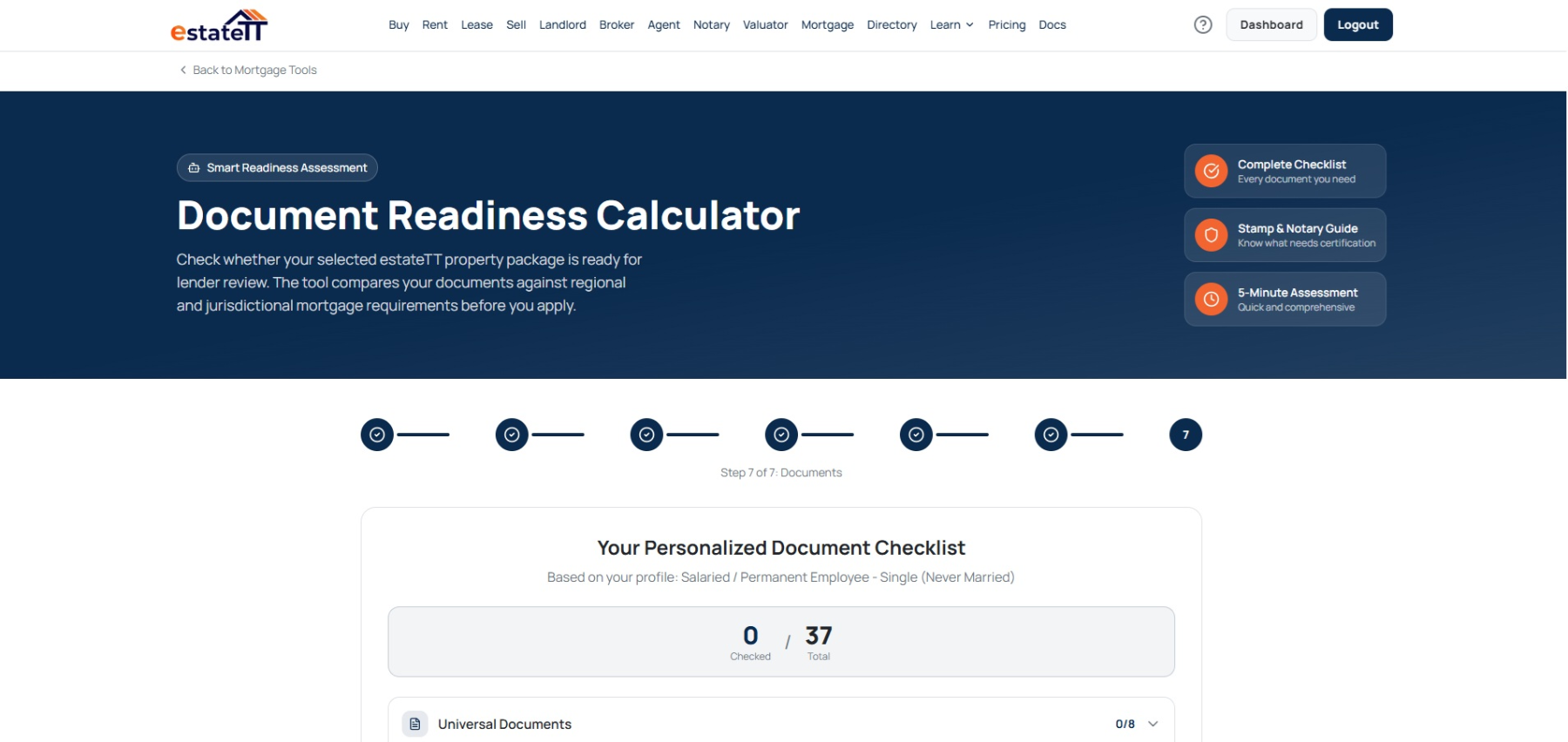

Preparing for a mortgage in Antigua and Barbuda? Find the document gaps before lender review.

Choose the property, describe your buyer situation, and check what you already have. estateTT builds a personalized document checklist, shows what is missing, and gives the preparation a place to continue when you are ready to save it.

estateTT mortgage readiness tool

A checklist shaped by the buyer and property

Choose

Link the property

Describe

Add your context

Check

Mark documents ready

Review

See gaps and priorities

Save

Continue in your account

The tool starts with context

Build the checklist around the Antigua and Barbuda purchase you are preparing for.

A generic mortgage list cannot know whether your property, residency, employment, or deposit context needs a different set of supporting records. The assessment starts with those details.

You can complete the assessment and see the result before creating an account. The account becomes useful when you want to save the assessment, upload documents, manage package progress, or control what a lender can see.

01

Start with the property and country

Select an estateTT listing and confirm Antigua and Barbuda as the property country so the checklist is attached to the purchase you are actually considering.

02

Describe the buyer behind the application

Residency, employment or company structure, relationship status, property type, deposit sources, and additional circumstances can change which preparation questions appear.

03

Mark what is already ready

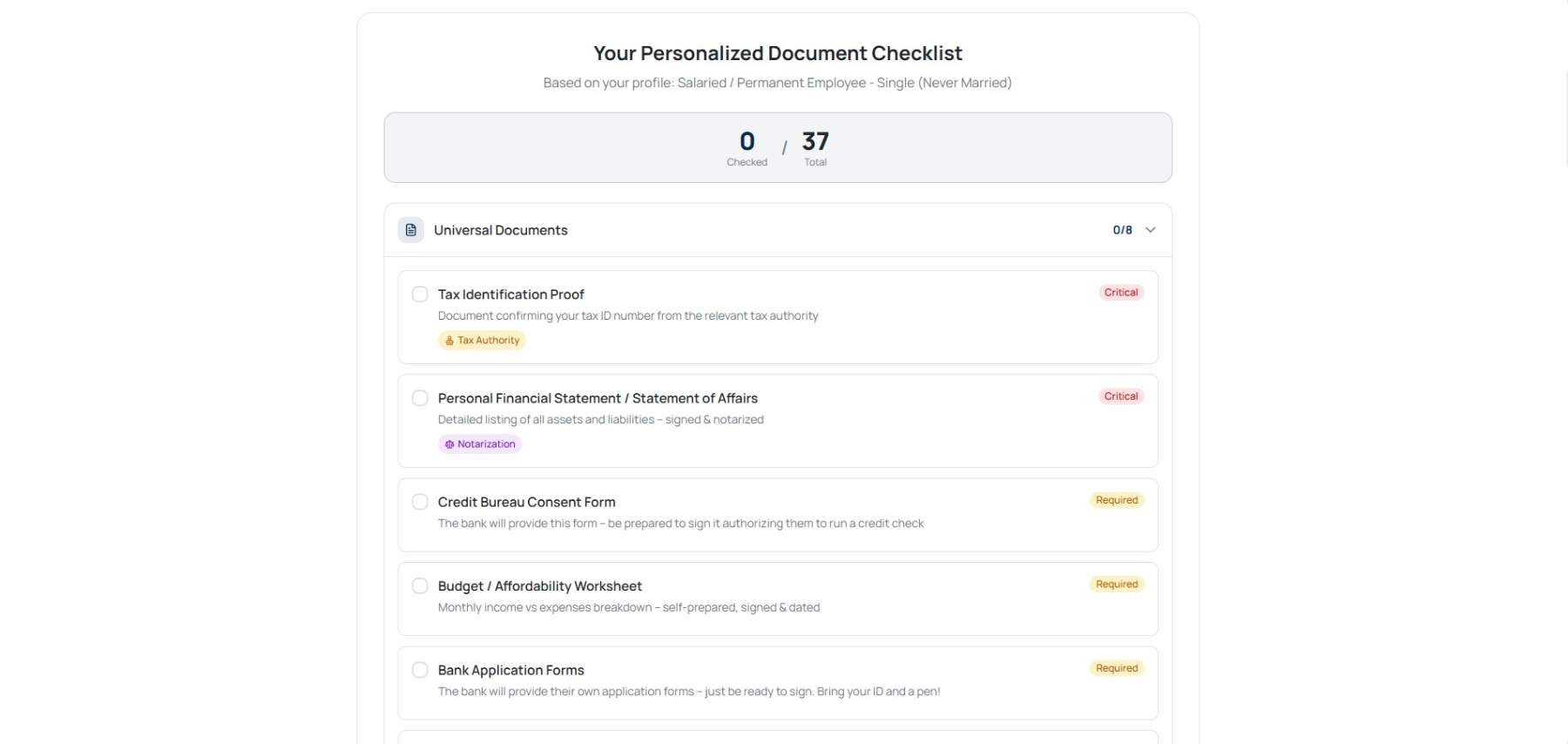

Work through the personalized checklist and mark the documents you already have. The result separates document completion from the higher-risk gaps that deserve attention first.

Your personalized document checklist

The result earns the next click

See what is ready, what is missing, and where to work next.

The assessment turns what you mark into a readiness view. It does not predict approval; it makes the next preparation step easier to choose.

Assessment first. Account when it becomes useful.

The checklist answers today’s question. The buyer account carries tomorrow’s work.

Complete the assessment and see its result before creating an account. If the package is worth keeping, the account turns that result into an ongoing readiness workspace.

Save the assessment

Keep the selected property, buyer context, checklist state, and readiness result.

Build the package

Upload supporting documents and return to package progress as gaps are resolved.

Control later access

Manage bank visibility, contact access, and document grants through package consent controls.

Readiness is not approval

Use the tool to prepare the conversation—not to replace the people making professional decisions.

Lenders, attorneys, valuators, and other qualified professionals remain responsible for their own decisions and requirements.

Lender

Sets its document requirements, assesses affordability and credit, and makes every lending decision.

Qualified professionals

Handle legal, title, transaction, valuation, and other professional work within their respective roles.

estateTT

Builds the preparation workflow, records what you mark ready, and keeps the package organized under your control.

Inside an eligible saved package

Use the saved package when document review becomes real work.

After saving, the buyer workspace can hold document uploads, package progress, corrections, consent controls, and a package-scoped document readiness AI agent. Access depends on the account and package state.

A later layer—not the hero promise

Use AI after the package exists and the visible facts have somewhere controlled to live.

What the package can help surface

- Save the assessment instead of rebuilding it

- Upload and organize supporting files

- Keep sharing under your control

The next useful route

Keep the mortgage question connected to the Antigua and Barbuda property decision.

Use the next route that answers the question now shaping the purchase: monthly payment, available property, or valuation context.

Mortgage calculator

Estimate a monthly mortgage payment separately from the document-readiness assessment.

Property for sale

Browse Antigua and Barbuda sale listings and choose the property you want the readiness work to support.

Property valuation

Prepare the property context for a qualified valuation conversation without treating asking price as a professional opinion.

Questions before you start

Using the Antigua and Barbuda mortgage readiness tool

Can I use the assessment without an account?+

Yes. You can complete the assessment and review the checklist and readiness result before creating an account. A buyer account is required when you want to save the assessment and continue with document uploads and package management.

Does the readiness score mean my mortgage will be approved?+

No. The score reflects the document information marked in the estateTT assessment. It is not a credit decision, pre-approval, lending recommendation, or promise that a lender will accept the package.

What does the assessment use to personalize the checklist?+

The workflow uses the property and jurisdiction, residency or incorporation context, employment or entity structure, relationship status, deposit sources, property type, and additional circumstances you select. Your lender remains responsible for stating its actual requirements.

Can I share the package with a lender?+

A saved readiness package can support bank visibility, contact requests, and document grants through account consent controls. The readiness tool itself does not submit a mortgage application, and you decide what access to grant.

Does estateTT provide financial or legal advice?+

No. estateTT provides readiness, organization, and workflow tools. Lending decisions, credit reporting, valuation conclusions, title work, and legal advice remain with the relevant institutions and qualified professionals.

The useful first step is already built

Start with the checklist. Create the account when the work needs to continue.

Run the Antigua and Barbuda readiness assessment, see the gaps, and decide whether the result is worth saving into your buyer workspace.

estateTT is a technology provider that delivers specialized workflow and organization tools for real estate platform participants in Antigua and Barbuda. estateTT is not a real estate agency, brokerage, legal firm, or financial institution. The platform does not make title, lending, landholding-license, fee, deposit, or transaction-outcome decisions. While the platform reserves the right to review participants to maintain network quality, it does not certify professional credentials or replace independent checks. Users are solely responsible for independently verifying all transaction details, licensing, and legal requirements with qualified local professionals and relevant Antigua and Barbuda regulatory authorities before engagement.